The accounting cycle is a series of steps that businesses take to track transactions and consolidate financial information over a specific accounting period (month, quarter, year). The end result of the accounting cycle is the production of accurate financial statements for that period and preparedness for the next accounting period. We will examine the steps involved in the accounting cycle, which are: (1) identifying transactions, (2) recording transactions, (3) posting journal entries to the general ledger, (4) creating an unadjusted trial balance, (5) preparing adjusting entries, (6) creating an adjusted trial balance, (7) preparing financial statements, (8) preparing closing entries, and (9) preparing the post-closing trial balance.

Identify transactions

Transactions involve buying or selling something and can be defined as ‘the act of conducting business.’ This could involve the exchange or transfer of goods, services, or funds. When a transaction occurs, it is recorded in the company’s accounting system, in the form of a journal entry. However, the transaction must first be identified; for example, if a company purchases machinery, they must add a new asset to the accounting equation.

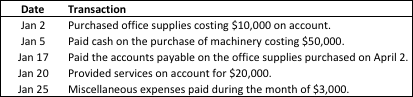

Identify transactions – example

On January 1, 2018, Martin Company issued 5,000 shares of common stock for cash at $20 per share. The company also identified the following transactions in January:

Failing to identify transactions would cause the subsequent steps in the accounting cycle to be inaccurate. Therefore, all transactions must be identified and analyzed or else we will have a flawed financial reporting process.

Effects of Transactions on the Accounting Equation

Each new transaction changes a company’s financial condition and impacts certain asset, liability, and/or equity accounts. The accounting equation is written below:

The accounting equation can be written as:

Assets = Liabilities + Shareholder Equity

The accounting equation will always hold true – if it does not, there is a problem. Properly recorded transactions will keep the accounting equation balanced. This is why it is important to not just identify, but also analyze transactions and record them accurately.

Record transactions

Transactions are first recorded in an accounting system in the form of journal entries. Each transaction must be listed in the appropriate journal and maintained in the order that they occurred. Each journal entry consists of the following information:

- The account(s) and amount(s) to be debited

- The account(s) and amount(s) to be credited

- The date of the transaction

- An explanation of the transaction

The following example will demonstrate the recording of the transactions we identified in the first step of the accounting cycle.

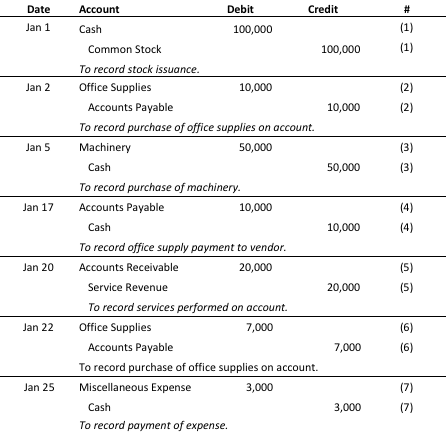

Record transactions – example

Each transaction has a debit and a credit entry, is listed in chronological order, and includes a brief description of the transaction itself. Now that each transaction has been properly recorded in the general journal, we are ready to post the journal entries to the general ledger.

Post journal entries to ledger accounts

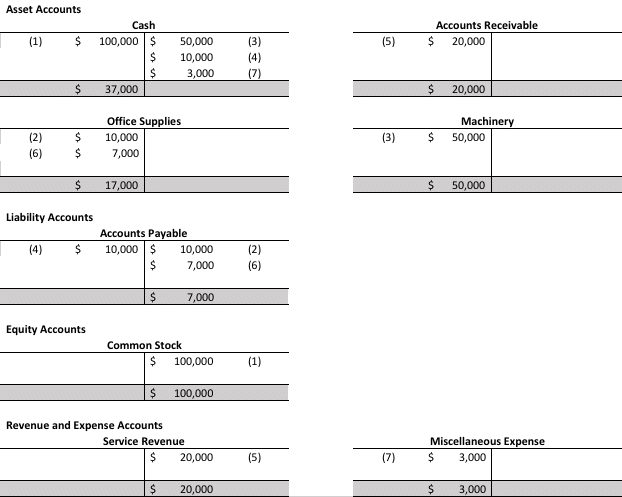

The general ledger is used to create a company’s financial statements. Once a transaction has been journalized, it is eventually posted (or transferred) to the general ledger. Having a complete listing of transactions in the general ledger will allow us to create the unadjusted trial balance and continue with the steps in the accounting cycle. The following example will demonstrate how we post journal entries from the previous step to the general ledger.

Post journal entries to ledger accounts – example

The ending balance in these ledger accounts (in grey) will be used to create the unadjusted trial balance in the next step. Remember: if the trial balance does not balance, something is wrong!

Prepare unadjusted trial balance

At the end of an accounting period, an unadjusted trial balance is created to verify that the total debit entries equal the total credit entries. The unadjusted trial balance is a list of accounts and their balances before any adjusting entries are made to create the financial statements. We will create the unadjusted trial balance by simply entering the ending balances in the ledger accounts from the previous step and adding up the debits and credits to see if they balance.

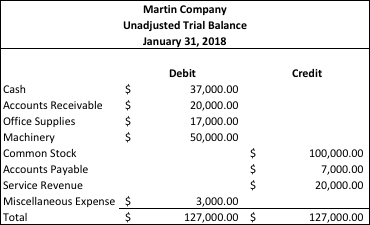

Prepare unadjusted trial balance – example

Looks good! Everything balances and this prepares us to make any necessary adjusting entries to create the adjusted trial balance.

Prepare adjusting entries

Adjusting entries are made at the end of an accounting period (year, quarter, month). These entries alter the final balances of certain ledger accounts to reflect the revenues earned and expenses incurred during an accounting period. This ensures that we comply with the accrual concept of accounting.

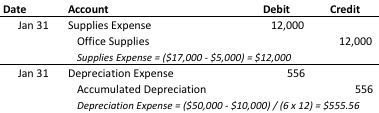

Prepare adjusting entries – example

Information for Adjusting Entries:

- Office supplies with an original cost of $5,000 were unused at the end of the period. Office supplies having an original cost of $17,000 are shown on the unadjusted trial balance.

- The machinery costing $50,000 has a useful life of 6 years and an estimated salvage value of $10,000. The straight-line depreciation method is used.

These adjusting entries will be used to adjust the trial balance to reflect changes that need to be made at the end of the accounting period.

Prepare an adjusted trial balance

After adjusting entries have been made, companies prepare an adjusted trial balance. The adjusted trial balance shows the balance of all accounts and includes the adjustments made at the end of the accounting period. In the following example, we will apply the adjusting entries made in the prior step to our unadjusted trial balance.

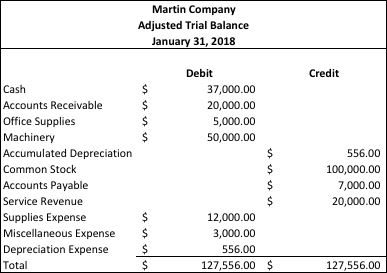

Prepare an adjusted trial balance – example

As you can see, ‘Supplies Expense’ increased by $12,000 and ‘Office Supplies’ decreased by $12,000 to reflect an expense we incurred in January, but had not yet recorded. ‘Depreciation Expense’ increased by $556 and ‘Accumulated Depreciation’ increase by $556.

Prepare financial statements

Financial statements can be prepared from the adjusted trial balance. Financial statements provide reporting on a company’s financial results, financial condition, and cash flows.

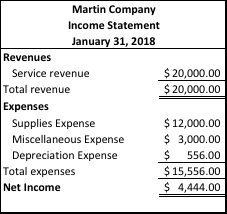

Prepare financial statements – example

Income Statement

Balance Sheet

Prepare closing entries

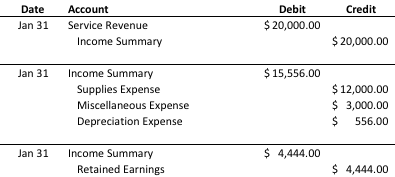

In the closing phase of the accounting cycle, the balances of temporary accounts are brought to zero to prepare for the next accounting period. In this step, temporary accounts are essentially ‘emptied out’ into permanent accounts.

Prepare closing entries – example

Prepare a post-closing trial balance

The post-closing trial balance eliminates all temporary accounts and leaves only real (or ‘permanent’) accounts. This balances allows us to check our work and determine that we journalized and posted the closing entries properly. The post-closing trial balances can be seen in ‘Step 7’ above as one of the financial statements we created.

Pop Quiz

[mlw_quizmaster quiz=194]