How Canadian Taxes Impact Your Personal Finances

You deal with Canada’s tax system long before you file your first return. Every paycheque, store receipt, and government benefit notice reflects tax rules that affect how much money you keep and what you owe. Understanding the basics helps you calculate your take-home pay, spot mistakes, and claim benefits you may already qualify for.

The federal government collects income tax through the Canada Revenue Agency (CRA). When you shop, sales tax depends on where you live—Ontario, BC, Quebec, and the territories do not all use the same system. If you live in Quebec, you also file a provincial return with Revenu Québec, and your paycheque may list QPP and QPIP instead of CPP and standard EI labels. Everywhere else in Canada, CPP and EI are the usual payroll deductions you will see.

Historical and Contemporary Milestones

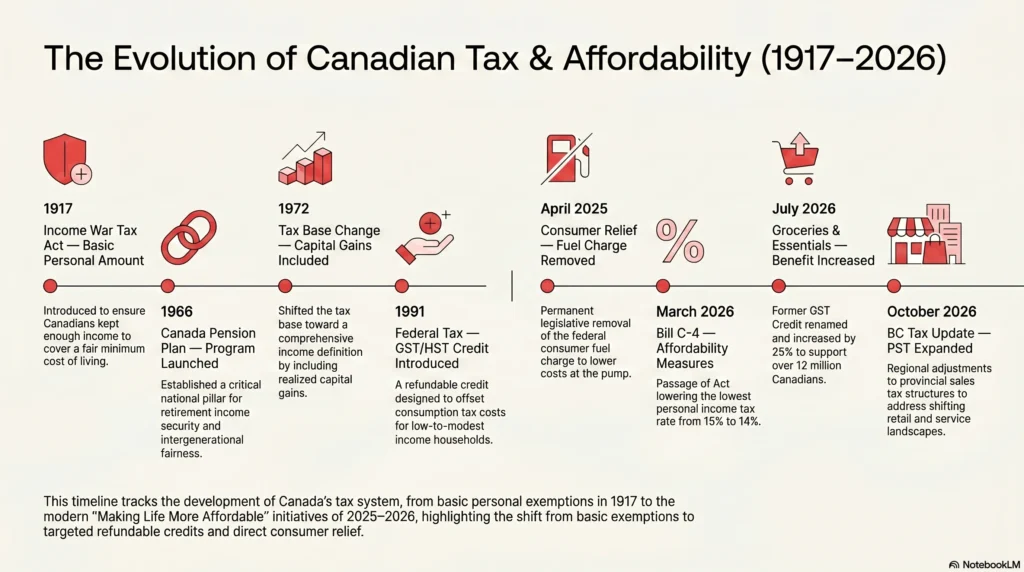

Canada’s federal income tax dates to 1917, when the Income War Tax Act created the Basic Personal Amount—the threshold below which you owe no federal tax on employment income. In early 2026, Bill C-4 lowered some taxes and added relief for families hit hard by living cost increases. By the time you file, the numbers may have changed again, but the habit stays the same: check the current rules instead of assuming what you heard last year still applies.

Below are some historic and recent changes to Canadian income tax policies.

Personal Finance Laws and Compliance

Canada’s tax system only works when people report honestly. You are expected to report all taxable income, claim only the deductions and credits you qualify for, and keep records that back up what you file. False reporting can trigger penalties and interest. In case you’ suspected of tax fraud, you may be audited, so keep the original copies of your financial records for at least seven years.

That is a lot to manage on your own. Governments know it, which is why they keep trying to simplify filing.

The 2025 federal budget put $71 million over five years toward automatic tax filing and automated federal benefits. Starting with the 2026 tax year, roughly one million lower-income Canadians with simple tax situations should receive pre-filled returns filed on their behalf. By the 2028 tax year, that number is expected to reach 5.5 million. This is not a new problem. In 2015, an estimated 10% to 12% of Canadians never filed a return, leaving unused benefits and credits ‘on the table’. The CRA tested an automated phone service called SimpleFile in 2018, but by 2023 only 7% of eligible callers used it, so they ended the service.

If you need help filing your taxes, you have several options. Community tax clinics, Indigenous tax service organizations, and official CRA or Revenu Québec resources exist so you don’t have to guess. Go to canada.ca or revenuquebec.ca before relying on something you see on social media or hear from people you know.

Payments in Lieu of Taxes (PILT)

Under Section 125 of the Constitution Act, 1867, the federal and provincial governments are immune from paying each other’s taxes. Because municipalities are created by provincial law, they cannot collect standard property tax on federally owned land, like a post office or a military base. Those properties still use municipal water, sewer, garbage collection, and roads like any other address in town.

Since 1950, the federal government has paid grants called Payments in Lieu of Taxes (PILT) so municipalities are not left covering the full cost of services to federal properties. Public Services and Procurement Canada distributes roughly $560 million each year across about 14,000 federal properties to more than 1,100 local taxing authorities.

Municipalities must apply for PILT annually and submit their local tax bylaws along with a list of federal properties within their borders. Federal payments are generally meant to approximate what property tax would have been on those lands. You will not apply for PILT yourself; it is an arrangement between federal and local governments that explains why federal buildings sometimes appear in local budget debates.

International Tax Rules

Canada also maintains rules to keep tax revenue from draining offshore. Think of them as guardrails on a highway: most drivers stay in their lane, but without barriers a few would cut across the median.

In 1972, Parliament limited how much debt foreign-owned companies could use to shrink taxable profits in Canada, and introduced a departure tax for people who leave the country while still holding significant assets. Further anti-avoidance rules followed in 1984, and in 2016 Canada joined an international agreement to coordinate treaty rules against profit shifting.

If you are filing a straightforward T4 from a part-time job, you will not use these rules directly. However, if you invest outside Canada, inherit assets abroad, or move overseas while still holding Canadian investments, you’ll want to review your tax situation.

Consumption Taxes Across Canada

Income tax is only half the picture. You pay consumption taxes almost every time you buy something.

The federal Goods and Services Tax (GST) is 5% nationwide. After that, your province decides whether provincial tax is blended in (HST), added on top (PST/RST), or added on top. In Quebec, you are also charged a Quebec Sales Tax (QST) and certain excise taxes on specific goods.

Other provinces mix GST with their own systems:

| Region / System | How consumption tax works at checkout |

|---|---|

| Ontario and the Atlantic provinces | use Harmonized Sales Tax (HST), which blends federal and provincial tax into one line at checkout. |

| Manitoba and Saskatchewan | charge separate Provincial Sales Tax (PST) or Retail Sales Tax (RST) on top of GST. |

| British Columbia | uses a dual system: 5% GST plus 7% PST on most goods—12% combined. GST and PST are each calculated on the pre-tax price, not stacked on each other. Printed books, children’s clothing, and bicycles often carry GST only; basic groceries and prescriptions are fully exempt. |

| Territories | charge GST only; there is no territorial sales tax equivalent. |

Do not memorize rate tables like this one. They change all the time. Search “sales tax” on your province’s finance site or canada.ca when you need current numbers.

Tariffs

Tariffs are border taxes on imported goods—you rarely see the word at checkout, but they can raise business costs and, eventually, shelf prices when countries like Canada and the United States impose trade measures on each other’s steel, vehicles, or food. That is different from GST, HST, PST, or QST, which apply at the register under rules your province sets.

What Gets Taxed and What Does Not

Sales tax rules treat essentials differently from everyday shopping. Basic groceries, prescription drugs, and most medical, dental, and educational services are zero-rated or exempt under federal rules in many provinces. Quebec is the main exception you should know: books are exempt from QST only—GST still applies. When you are unsure, check your receipt or look up the item on canada.ca (or your provincial revenue site).

Housing Affordability and the First-Time Home Buyers’ Rebate

Two partners save for three years and sign an agreement on a newly built condo priced at $485,000.

Before March 20, 2025

Federal GST on that purchase would have added roughly $24,250 to their closing costs.

On or after March 20, 2025 (Before 2031)

Under the First-Time Home Buyers’ Rebate, agreements signed between these dates will have the 5% GST removed on new homes up to $1 million.

For our example, that policy difference can mean keeping roughly $24,250 in their down-payment fund instead of paying it as federal GST at closing. The rebate does not make housing affordable on its own. It removes one major cost from an already expensive purchase.

Canada Groceries and Essentials Benefit

Starting in July 2026, the Canada Groceries and Essentials Benefit will increase payments by 25% for five years, building on the existing GST/HST credit system. If you qualify, the extra amount arrives through the same quarterly deposit rhythm. The credit is designed for lower income families: though it’s not much per quarter, this benefit is meant to offset some of the sales tax you pay on everyday purchases.

Reading Your Pay Stub

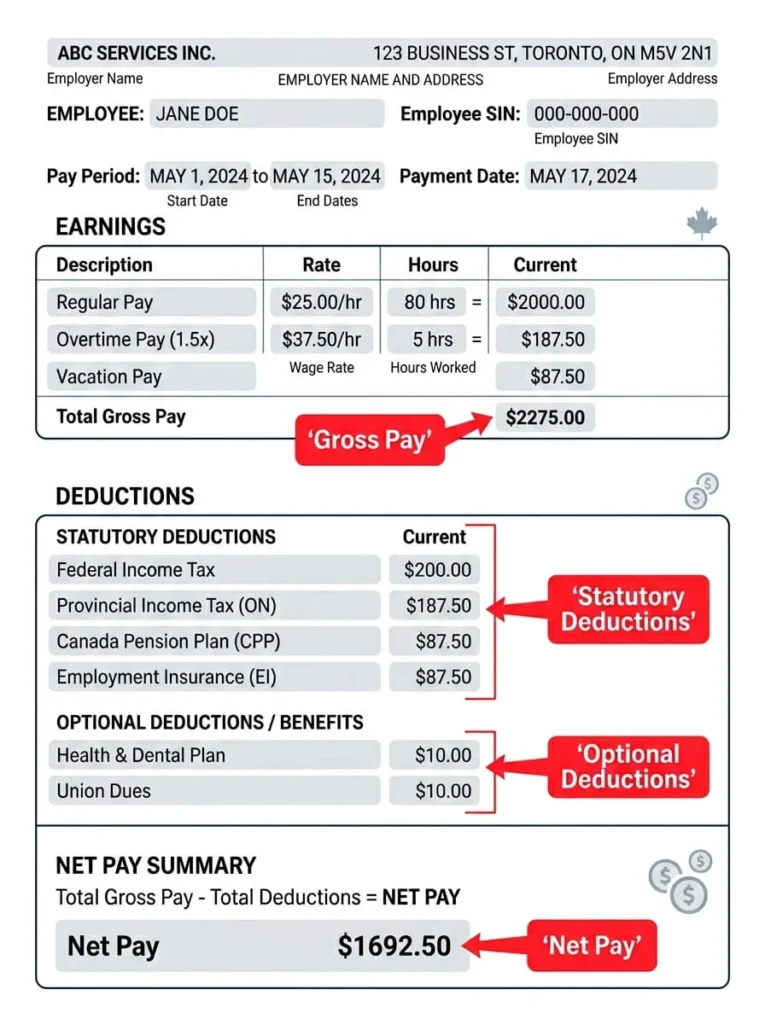

Looking at your first pay stub can sting. The total at the top is not what lands in your bank account, below we review the different deductions you

Start at the header. You should see your employer’s name, the pay period dates, your hourly rate or salary, and hours worked if you are paid by the hour. Gross pay is everything you earned this period before anything comes out—wages, salary, overtime, and commissions if your job pays them.

Below gross pay, deduction lines tell the story.

Outside Quebec

On a federal-style stub, expect income tax withheld, CPP contributions, and EI premiums, plus any voluntary items your employer deducts.

Quebec

In Quebec, the same lines may read QPP and QPIP instead of CPP, with QST-related payroll items where applicable.

Net pay is what actually lands in your account. Budget from that deposit, not from the hourly rate on your offer letter. A $18-per-hour job does not put $720 in your pocket every forty-hour week once statutory deductions and optional plans come out. Plan rent, transit, and spending from the deposit amount. That habit helps you avoid overdrafts and scrambling before payday.

At year-end your employer sends a T4 slip. It totals your taxable income and every dollar withheld for CPP (or QPP), EI, and income tax across the calendar year. You need that slip to file your return.

Payroll Calculations and Deductions at Source

Statutory deductions are amounts your employer must withhold by law: income tax, CPP or QPP, and EI or QPIP in Quebec. They fund programs you may draw on later—retirement, parental leave, unemployment—and they prepay your income tax so you are not hit with one giant bill in April. Income tax withholding follows federal and provincial brackets set in law; when rates change, your employer’s payroll system applies the current tables.

Other deductions are optional or employer-specific: union dues, health and dental plans, uniform costs, charitable donations through payroll, and sometimes provincial payroll taxes. Each line on your stub should have a label. If you do not recognize one, ask your payroll department to clarify before you receive your next paycheck.

Step-by-Step Payroll Calculation

Suppose you work 40 hours at $20 per hour, bringing your starting gross pay to $800.

1. Subtract Statutory Deductions

- Federal & Provincial Income Tax: $85.00

- Canada Pension Plan (CPP): $41.00

- Employment Insurance (EI): $13.00

- Total: $139.00

2. Subtract Optional Deductions

- Union Dues: $12.00

- Extended Health & Dental Plan: $15.00

- Company Pension Contribution: $20.00

- Total: $47.00

3. Calculate Your Net Pay

- Net Pay = Gross Pay − Statutory Deductions − Optional Deductions

- Net Pay = $800.00 − $139.00 − $47.00 = $614.00

This is the total amount that will be deposited in your bank account. This is what you should use for any income calculations in your budget.

Banking and Work Incentives

NSF fee cap (March 2026)

A $10 cap on non-sufficient funds (NSF) fees took effect in March 2026, limiting how much banks can charge when a pre-authorized debit bounces.

Canada Workers Benefit (CWB)

The Canada Workers Benefit (CWB) is a refundable tax credit for workers aged 19 and older who earn at least $3,000 in employment income. You claim it on your return; it can boost a low income even when little tax is owed.

Pay Equity

Two coworkers train for the same role, carry the same responsibilities, and deliver work of equal value. Should pay differ because of gender?

Pay equity exists to prevent that outcome. Its purpose is equal pay for work of equal value without regard to gender. It does not guarantee every employee in a company earns the same dollar amount—different jobs can still pay differently—but it blocks gender from being the reason two equally valuable jobs pay unequally.

If you suspect a pay equity violation, workplace complaint pathways exist through employers, human rights commissions, and labour standards offices. For enforcement detail, see Workplace Rights, Safety, and Equity in Canada.

Indigenous Perspectives and Treaty-Related Income

First Nations, Métis, and Inuit communities carry distinct legal and constitutional histories that shape how income is taxed in specific situations. Treaty-related income does not follow one national rule. Treatment depends on your status, the treaty or agreement involved, and where the income was earned—especially whether activity occurred on or off reserve. Under Section 87 of the Indian Act, employment income earned by a registered status Indian is exempt from income tax if the work is performed on a reserve, whereas the exact same type of work performed off-reserve remains fully taxable.

This lesson cannot replace advice from someone qualified to work through your situation. Indigenous Services Canada, local band offices, and Indigenous tax clinics can connect you with benefits information, clinic dates, and referrals. Ask early rather than assuming your summer job is taxed the same way as your friend’s.

Reserve lands and federal properties are exempt from municipal property tax under the Constitution Act, 1867. Municipalities still need revenue to operate. PILT grants, described earlier, are one way the federal government backfills part of that gap.

Substantial Financial Gains

Imagine you won $50,000 from a lottery, or inherited a lump sum from a relative, or you received a bonus equal to three months of pay. Your brain might just immediately to your next shopping trip. Before you get carried away, take a moment to review your new financial situation.

We recommend using the PAUSE checklist:

- P: Preserve your financial records. Write down where the money came from, the date you received it, and any tax forms attached.

- A: Allocate to an emergency fund before you upgrade your lifestyle.

- U: Understand your new tax situation. A windfall is often taxable; know what you may owe before you start spending.

- S: Set a waiting period before making any major purchases. Many advisors suggest waiting 30 to 90 days after receiving a large sum of money.

- E: Engage qualified help. A tax clinic, accountant, or financial advisor costs less than a rushed mistake.

Lottery fantasies are fun; tax bills and empty accounts are not. Make sure you understand how much money you will be able to keep, and always think about replenishing or expanding your emergency savings before you start spending.

Government Programs and Your Retirement

Old Age Security began in 1952, paying $40 a month to seniors aged 70 and older. The Canada Pension Plan launched in 1966. The Guaranteed Income Supplement followed in 1967 to support low-income seniors. Together they form a floor—not a furnished apartment.

OAS, CPP (or QPP in Quebec), and GIS were never designed to replicate your full working income. By 2025 annual OAS spending reached $86 billion and is projected to hit $104 billion by 2029, reflecting an aging population. Governments adjust benefits, but demographics pressure the system. Relying on future politicians to fund your entire retirement is a bet you do not want to make.

What you can control starts now: contribute to CPP through every paycheque, save in an RRSP or TFSA when you can, and learn how employer pensions work before you need one. For career-long CPP/QPP contributions and retirement planning depth, see A Guide to Retiring in Canada.

The freedom you want at 65 is built from habits at 16—not from hoping a government cheque covers rent in a city where rent keeps climbing.

Staying Organized Year-Round

Tax season hurts less when you stop treating it as one night of panic. Keep T4s, receipts for deductions you plan to claim, and records of major financial moves in one folder—physical or digital. When you marry, separate, or have a child, tell the CRA by the end of the month following the change. If you separate, wait at least 90 days before notifying the CRA so the status is clear.

As of July 15, 2025, the Authorize a Representative function in EFILE software for individuals ended. Representatives now request access through the Represent a Client portal using tax information from a notice of assessment at least six months old. If you are locked out of your CRA account, new self-service recovery options can restore access without having to make a phone call.

The tax policies and rules are often changing, so make sure to check on canada.ca (or revenuquebec.ca) to understand your current situation fully. Remember there are many free community tax clinics who are here to help you if you have any questions.