Financial Resilience and Life Transitions

Jada graduated in May and moved back home with her parents. She found a part-time retail job and had a plan to move into her own apartment by fall. In June, her car needed a $1,400 repair. Then in the middle of July her hours were cut. In August she had less saved than she had hoped, and the apartment search now felt impossible. To add insult to injury, every friend posting move-in photos on social media made her current situation sting a little more.

Jada’s summer illustrates a major life transition. Major events—including graduation, a new career, relocations, or sudden job losses—instantly reshape your income, expenses, and priorities.

Financial resilience is your ability to adapt, recover, and keep moving when circumstances change. No one is able to predict every challenge that is coming their way. However, you can develop a plan that is flexible, and the self-awareness to know what is important for you. Over time you’ll build habits that help you respond without panic.

When faced with a major life change, pause before committing to new financial obligations. Calculate exactly how the change affects your monthly income and expenses. Inventory your personal resources so you know what tools you can use. By establishing a clear baseline, you will know exactly where to go next.

Personal Resources and Flexible Planning

Your personal resources are everything you can draw on to meet life’s demands: time, physical energy, emotional energy, knowledge, skills and talents, access to technology, and money. A personal resource plan—or financial plan—maps those resources to the lifestyle you want and can actually sustain.

Time

Money

Knowledge

Emotional Energy

Skills & Talents

Access to Technology

Physical Energy

Your values, priorities, and cultural background shape how you spend these resources. Societal norms dictate what a “successful” life looks like. In some communities, families pool money through informal savings groups or prioritize supporting extended relatives. In others, financial plans focus purely on the individual. Neither approach is inherently correct, but both fundamentally change your financial baseline.

Values-based planning requires you to ask a simple question: What matters most to me right now? Your answer will change as you mature. If your budget funds old goals you no longer care about while starving your current priorities, you must revise it.

Rigid budgets shatter during major transitions. When your life changes, you may need to pause your savings, redirect cash to basic survival needs, or focus entirely on rebuilding your emergency fund. Rebalancing your budget after a crisis takes time. Expect weeks or months of trial and error before your spending matches your new reality. Revisit your financial plan whenever your income, lifestyle, or goals change.

What Shapes Your Money Choices?

Two people with the same income can make completely different choices. Your choices reflect a mix of your family history, social circles, personal values, and psychological triggers.

Most people operate under invisible money scripts. These are unconscious beliefs about wealth, typically inherited in childhood by watching how adults managed money. For example, a script of extreme frugality might have protected your family during a difficult period. However, that same script can cause intense anxiety when you try to buy essential goods you can easily afford today.

As you gain financial independence, write your own financial philosophy. Base this philosophy on your personal values, family expectations, and long-term goals. Decide what you want your money to support, identify the trade-offs you are willing to accept, and recognize who you are trying to impress.

Preference-Driven

Preference-driven spending aligns directly with your personal values and long-term goals. You choose these purchases because they support what you actually care about, not because of external pressure.

This includes saving for a specific target, buying tools for your trade, or supporting your family. You would make the exact same choice even if no one was watching.

Pressure-Driven

Pressure-driven spending reacts to external forces, like a friend’s new purchase, a flash sale, or social anxiety. These decisions feel incredibly urgent in the moment but collapse once the pressure fades.

You likely would have ignored the item if your social media feed stayed quiet or the countdown timer disappeared.

The same purchase can be wise for one person and unwise for another depending on values and context.

Marketing tactics and social expectations rarely announce themselves. Advertisers use subtle psychological triggers—like artificial scarcity, social proof, and fear of missing out (FOMO)—to bypass your logic and trigger impulsive spending. For how marketers use these levers in ads and offers, see Consumer Psychology and Persuasion in Marketing. For how to manage your spending and catch overspending before it happens, see How Do You Stop Impulse Purchases?

Major life transitions often surround you with new peers, different advertisements, and shifting norms. While general marketing courses cover retail tactics, they often overlook a major internal trigger, mood-state spending.

Mood-State Spending

Stress, boredom, loneliness, or household conflict can trigger purchases that soothe your emotions for an hour but ruin your budget for a month. When you buy something after a difficult week, your purchase often has more to do with your emotional state than the product itself. Career transitions, sudden moves, or family disputes increase this risk—especially when online comparison wears down your resolve.

Your choices depend on market availability, marketing persuasion, and personal preference, not simply the price tag. Digital banking apps, budgeting platforms, and automated bill alerts can keep your finances on track. Choose simple tools that fit your existing habits rather than forcing yourself to use complex systems.

Lifestyle, Income, and Connected Goals

Your lifestyle is the daily expression of your needs, wants, and spending habits. To remain financially secure, your lifestyle expectations must align with your actual income, regardless of what your peers or social media algorithms label as “normal.”

Lifestyle creep occurs when your expenses rise alongside your income. A larger apartment, premium subscriptions, and frequent dining out feel entirely reasonable after you secure a raise. However, these small upgrades quickly absorb your new earnings, leaving your savings stagnant. Fixed, recurring commitments—like auto leases, rent hikes, or subscription contracts—are exceptionally difficult to cut if your income suddenly drops.

You must align your career goals with the cost of your desired lifestyle. Your education, career trajectory, and geographic location dictate your earning power. Remember that money is deeply connected to your education, family, and physical health. Following a major economic shock, redefine what success looks like. Rebuilding your emergency fund or stabilizing your basic cash flow is a massive victory, even if you must pause your long-term goals.

Top tip: Your mental health and your money are deeply connected. Financial anxiety can paralyze your decision-making, which often leads to costly mistakes. High-interest, predatory loans—like payday loans—always cost far more than the temporary relief they provide. Stress-driven spending offers a fleeting escape but leaves you with deeper anxiety when the bill arrives. Before you borrow or spend to cope with pressure, pause and ask if the decision will hurt your future self.

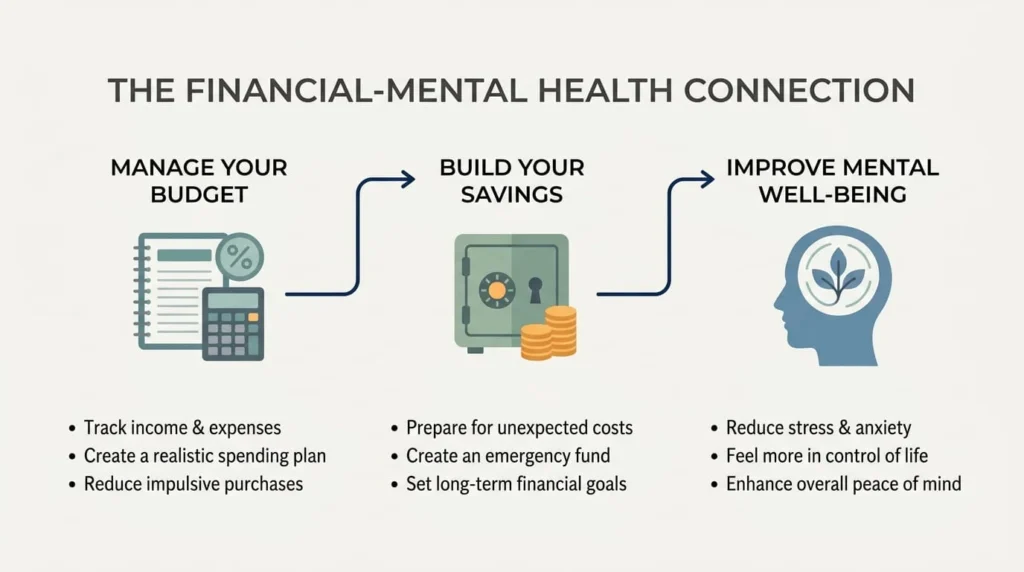

Financial Well-Being and Mental Health

True financial security underpins your mental well-being. Conversely, financial stress triggers a dangerous cycle: worry leads to impulsive, panicked money choices, and those choices worsen your financial situation. Debt and mental distress feed each other in a continuous loop.

Predatory, high-interest borrowing causes severe psychological distress compared to low-interest, structured loans. When your budget is tight, every transaction requires a painful trade-off. This constant mental load drains your willpower and processing power. If you feel overwhelmed, do not suffer in silence; reach out to trusted professionals or community support programs.

Life Changes and Coping Strategies

Major life changes will disrupt your financial baseline. Some of these transitions arrive with years of warning. Others strike in an instant.

To survive these shifts, you must plan ahead, build cash reserves, seek expert advice, and adapt your strategies as conditions change. After a major family transition like divorce or the death of a spouse, immediately take inventory of your assets, update your insurance beneficiaries, and review your new tax obligations. If you lose your job, focus your energy on separating your immediate survival needs from long-term career decisions.

Getting back on track is as much about not letting yourself be overwhelmed by shame, and allowing yourself to find solutions to support yourself in the short-term. Once things restabilize, you will feel have the mental clarity to see if your old goals are still valid, or if you want to go in a new direction.

Housing and Independent Living

Securing housing during a transition is a complex decision involving your personal values, timing, and market access—it is never just a math problem. You must weigh your geographic mobility, career changes, stress tolerance, and readiness to purchase a property. While local tax credits and government housing programs can expand your options, the core choice rests on your immediate lifestyle needs.

Stability

Homeownership can provide long-term stability and build generational wealth.

Flexibility

Renting provides geographical flexibility and shields you from expensive repair bills.

Neither housing option is purely financial. Historical and systemic discrimination—including redlining and Fair Housing Act violations—has locked marginalized communities out of affordable housing and generational wealth. If you suspect or experience housing discrimination, the U.S. Department of Housing and Urban Development (HUD) is here to support you.

When evaluating a new place to live, go around the neighborhood and talk to locals to find out if its safe, what the likely utility costs will be, and make sure you understand the terms of the lease or mortgage. Shared housing with roommates can cut your monthly expenses in half, but you must establish clear, written agreements regarding rent splits, utility bills, and household chores before moving in.

Independent living requires you to manage utilities, groceries, insurance, and emergency expenses on your own. If you move back in with your family to save money, establish clear expectations. While a “boomerang” move reduces your expenses, it can strain your personal boundaries. Set a firm move-out timeline, agree on household contributions, and view this transition as a temporary step toward your next goal.

As a tenant, you have legal rights and responsibilities, starting with paying rent on time and maintaining the property. If you reside in Washington, DC, the Office of the Tenant Advocate helps renters navigate legal disputes. If a conflict arises with your landlord, document every interaction, send all communications in writing, seek assistance from local legal aid agencies, and escalate your complaint through official channels if necessary.

Crises, Unexpected Expenses, and Rebuilding

Layoffs, medical emergencies, and sudden accidents can dismantle a budget overnight. To build a buffer against these shocks, check out How to Prepare for Unexpected Expenses.

When a crisis strikes, pause before making any major financial decisions. Avoid high-cost, predatory traps like payday lenders or title loans. Instead, work systematically through this response hierarchy: slash non-essential spending immediately, apply for community or government assistance, negotiate directly with your creditors, and borrow funds only as a last resort.

Many households in crisis survive by focusing strictly on the “Four Walls”: shelter, food, utilities, and basic transportation. Protecting these essentials keeps you safe and allows you to continue earning an income. If you face overwhelming debt, contact a nonprofit credit counseling agency to help you build a structured recovery plan.

Check out your local relief agencies like the Department of Human Services (if you live in Washington D.C.), which provides emergency utility and housing assistance. If you live elsewhere in the United States, dial 2-1-1 to connect with local aid programs, emergency grants, and free financial counseling services.

Your money management strategy must adapt to your current income level. When resources are scarce, focus entirely on your basic needs and your immediate emergency fund. If you experience a sudden income drop, direct every dollar toward survival before slowly rebuilding your cash buffer.

Going back to our example at the beginning of this lesson: after Jada’s manager cut her hours, she immediately paused her apartment search. She calculated her new monthly income, applied for temporary assistance to help with her student loans, and adopted a bare-bones budget until her shifts stabilized. By adjusting her goals to fit her new reality, she felt a lot less stress because she knew that she was working towards a sustainable lifestyle.