Why Invest in Stocks vs. Keeping in Savings?

Can’t view on YouTube? Click Here

Investing in stocks can be a great way to make your money work for you and build long-term wealth, once you have set up your budget and emergency savings fund. In this lesson, we’ll explore why investing in stocks is a smart financial decision for anyone looking to secure their financial future.

When you have a longer time horizon that you intend to keep your money invested for, like 20 years or more, the stock market historically has provided the greatest return.

A time horizon is a term used in finance and accounting to describe the length of time that an investment is held for. It’s like a timeline that refers to the amount of time you have to save for something like retirement or buying a house.

Most people keep their savings in a savings account at their local bank. Banks usually pay interest on the cash held in your savings account. So, if you have $1,000 in your savings account, and the bank pays you 3% interest, then at the end of the year you’ll have about $1,030.

Once your savings balance gets larger, a lot of people hope to earn more money than what the bank is paying in interest. This is when they’ll invest their money in assets like real estate, stocks, bonds, and/or gold.

Historical Returns of Investments

While no one knows for sure what will happen in the future, a look at historical returns shows how these different investments have performed over time.

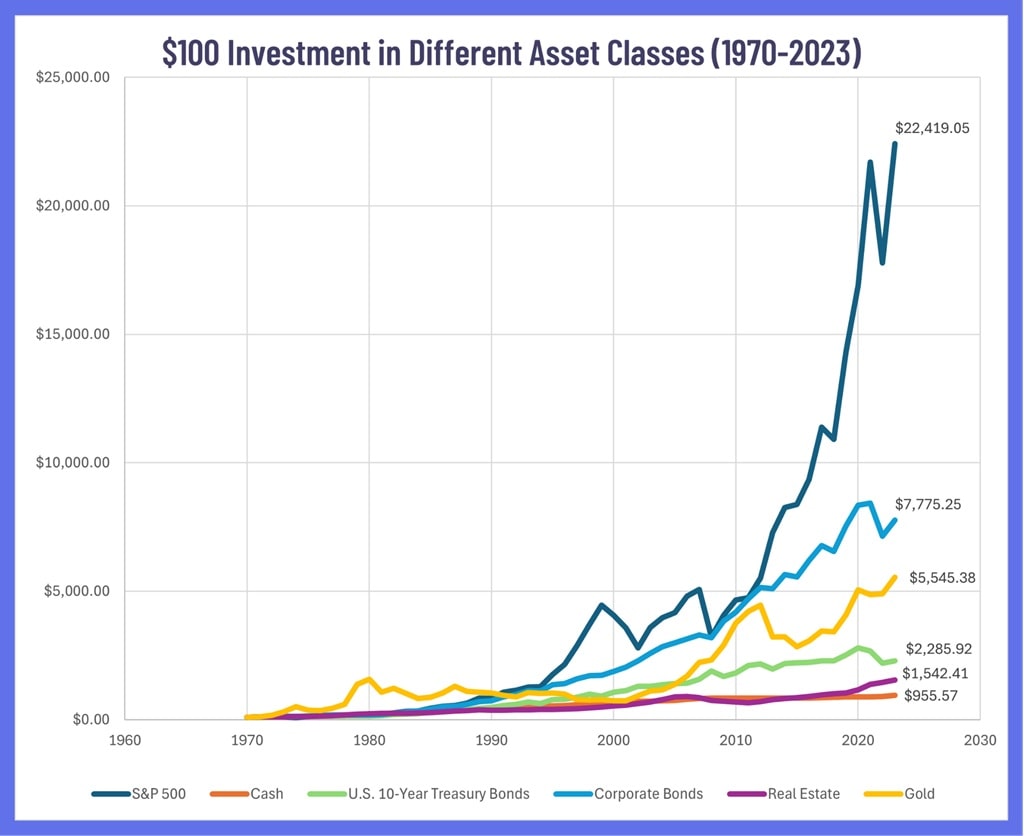

Here’s a chart of average percentage returns for $100 dollars invested in different assets between 1970 and 2023.

| Investment | Description |

| US Stock Market | The average of all stocks trading in the United States. |

| US Large Cap | The average return of the biggest companies in the United states, (e.g. Apple Inc., Microsoft Corporation, Alphabet Inc. etc.) |

| US Small Cap | The average of start-up companies, these have higher risk than bigger companies, but can also provide bigger rewards. |

| Short-Term Treasury | Short-term government bonds that are issued or guaranteed by the United States, with maturity lengths of 4, 13 or 26 weeks. |

| Long-Term Treasury | US government debt securities with a maturity date of 5 or more years, issued to finance the operations and meet the country’s financial obligations. |

| Long-Term Corporate Bonds | Bonds issued by companies for more than 5 years. The return is lower than stocks, but is also less risky since if the company goes bankrupt, bond holders get paid before stock holders. |

| High Yield Corporate Bonds | Bonds with either a very short duration (usually less than 5 years), or bonds on companies that are considered risky (they have a high chance of going bankrupt). |

| Real Estate | Investing in property and buildings, either to rent out or to re-sell at a higher price. |

| Gold | Buying physical gold (bullion coins, bars, jewelry), gold ETFs, gold mutual funds, gold futures etc. |

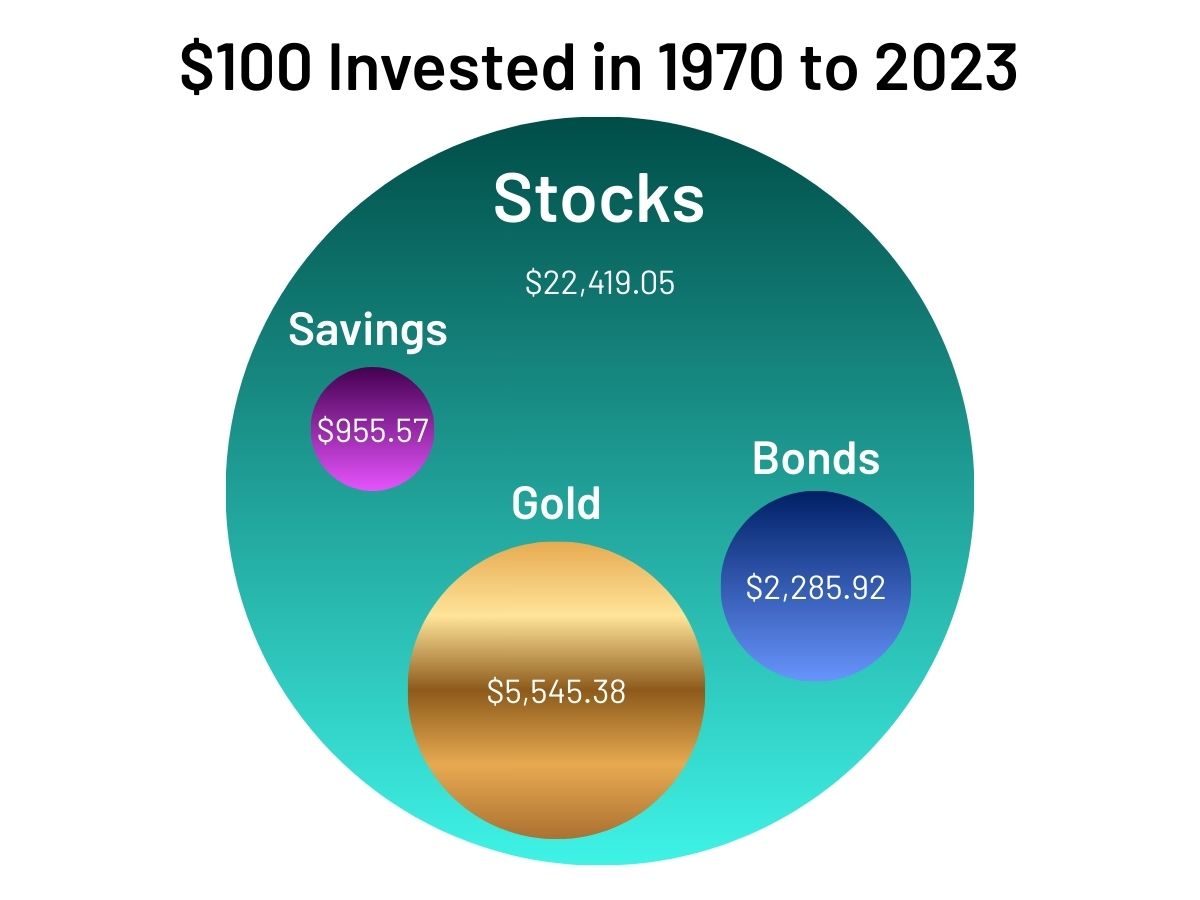

Over time, where you put your money makes a huge difference. The image you see shows the growth of a single $100 investment over the 53 years from 1970 to 2023, depending on whether it was put into stocks, gold, bonds, or a simple savings account.

Looking at this visualization, the stock market (represented by the S&P 500) was the clear winner. The initial $100 grew to over $22,000, which is a staggering increase of more than 22,000%. In contrast, leaving the money in a savings account (cash) performed the worst, growing to just over $955. Gold also performed well, turning $100 into more than $5,500, but it was still dramatically outperformed by the stock market over this long period.

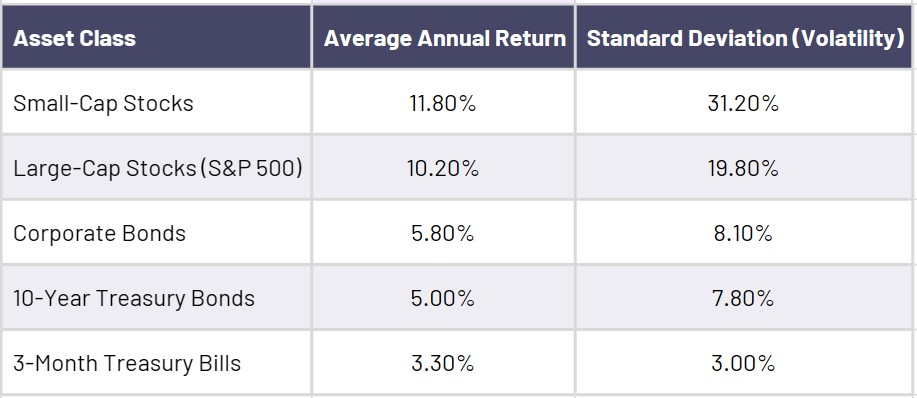

Historical Risk and Return

This table looks at the historical average returns of different investments. Over the long run, Small-Cap stocks have produced the highest average annual return at nearly 12%, closely followed by Large-Cap stocks (like the S&P 500) at around 10%. This is significantly higher than the roughly 5% return from safer investments like government bonds.

However, return is only half the story. The Standard Deviation column measures volatility—how much an investment’s value swings up and down. Notice that Small-Cap stocks have a massive volatility of 31.2%. This means that while the average return is high, the year-to-year results can be wildly unpredictable. In contrast, the 7.8% volatility for Treasury Bonds shows a much smoother, more stable journey.

This trade-off between risk and reward is important. Volatility is the price investors pay for the chance at higher returns. If you looked at just one year, or even five, the high volatility of stocks might lead to losses. However, the longer your time horizon is, the more time these swings have to average out and work in your favor, which is why stocks are considered the best tool for long-term goals like retirement.

Summary

If you want to maximize your personal net worth, if you want to be rich, if you want to be a millionaire, if you want to retire early, you must start saving and investing today.

The earlier you get started, the more time your money has to grow. And the more time it has to grow, the bigger it will become.

Understanding how the stock market works, and how to invest is so important because it determines how much your net worth will be when you retire. Are you going to leave your cash in your savings account all your life, and earn an average of 3%? Or are you going to invest it in the stock market and try to earn a higher return?