Preparing for Retirement – IRA and 401(k) Plans

The earlier you start saving for retirement, the more comfortable you will be when you get there. Compare two people:

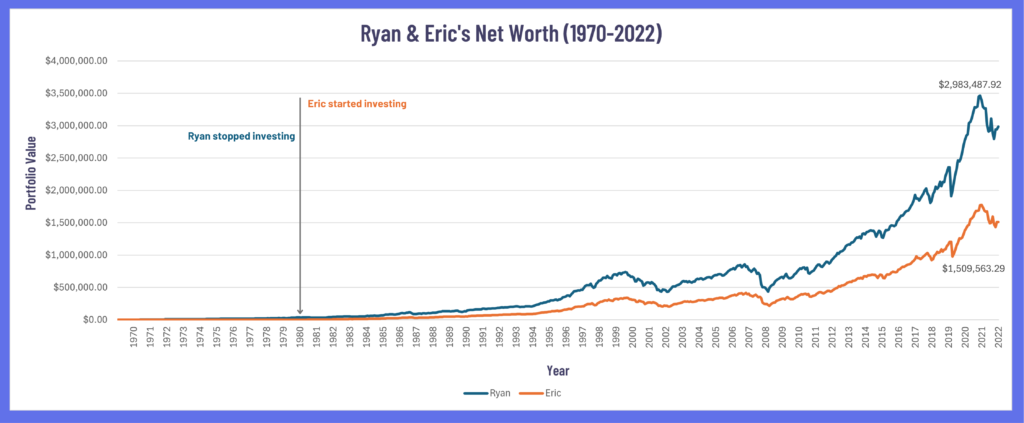

Ryan

- Starts investing $167/month ($2,000 per year) from age 16 until 25.

- From age 26 onwards, spends everything he earns (no savings/investing)

- Total amount invested: $20,000 ($2,000/year for 10 years)

Eric

- Spends everything he earns until he turns 26.

- Starts investing $167/month ($2,000 per year) from age 26 until 65.

- Total amount invested: $80,000 ($2,000/year for 40 years)

Thanks to the power of compound interest, Eric’s retirement portfolio never catches up to Ryan – in fact he doesn’t even come close. Using the actual market returns from 1970 to 2022, Eric would finish with just over $1.5 million in his retirement account, but Ryan will have nearly $3 million – twice as much money for one quarter of the total investment.

The extremely strong importance of investing early led to the creation of special retirement plans to encourage saving – IRA and 401(k) plans. Both plans are designed to give you free “bonus money” just for making early and consistent retirement contributions.

IRA vs 401(k)

Both of these are tax-advantaged retirement programs. This means that you get tax breaks for contributing – so contributing $100 might only “cost” you $90 (or less) once taxes are considered. IRA plans are available for anyone, but 401(k) plans must be offered by an employer.

IRA – Individual Retirement Arrangements

Can’t view on YouTube? Click Here

An IRA plan can be opened by any individual. You can contribute up to $7,500 to an IRA account every year, which can then be invested in virtually any method you wish (stocks, bonds, mutual funds, even crypto or real estate, depending on the type of retirement account).

When you file your taxes, any contribution (up to the $7,500 limit) is deducted from your “taxable income” – so any tax you would have paid on that contribution is free money for you!

401(k) Plans

Can’t view on YouTube? Click Here

401(k) plans are offered by an employer as part of a company’s benefits package. A 401(k) plan has an added incentive for saving – every time you contribute to your 401(k), your employer also contributes a matching amount, up to some percentage of your base salary (typically 3-5%). Like the IRA, you when you file your taxes you can deduct any 401(k) contributes from your taxable income.

This is a big deal – it means your employer is effectively doubling every contribution you make, AND you get a tax break on top of it! That’s free money on top of free money – but you can only get it if you make your regular retirement contributions.

401(k) contributes are typically automatically taken out of each paycheck, at some point below or up to your employer’s match. However, employees have the option to change this to contribute more (or less) than the company’s automatic enrollment setting.

Unlike an IRA, what you can invest with your 401(k) account is restricted to whatever investments are offered through your company (typically funds and bonds, but many companies also allow investments in individual stocks). However, if you leave an employer, you can take your 401(k) account with you (with some restrictions) – including converting it directly into an IRA account.

Traditional vs Roth

Both IRA and 401(k) plans have two “flavors” – Traditional and Roth. Traditional accounts work exactly as described above – you can deduct any contribution from this year’s income for an immediate tax break (and free money).

A Roth type account does not give you any immediate tax break – but when you withdraw from your account after retirement, you will pay no income taxes on your earnings.

There is no right or wrong choice for “Traditional” vs “Roth” – it comes down to how important that “free money” is today vs how much you think you will need it in retirement.

This simulation does not have any mechanism for IRA or 401(k) accounts – all savings you choose to make is entirely at your discretion.