A Registered Education Savings Plan (RESP) is a Canadian savings account built for post-secondary education. Parents, guardians, or other contributors deposit money over many years, and the federal government may add matching grants on those contributions. When you enroll in an eligible program, those funds can help pay for tuition, rent, books, and other school costs. An RESP is savings you already have, not a loan.

Below, you’ll see how to layer the funding sources available to Canadian students—from grants and government aid to campus work—so you can choose a mix that fits your situation and keeps borrowing as low as possible.

How Much Does It Cost?

Registration and tuition fees are not fixed nationwide. They shift with the level of education (college versus university), the program you choose, whether the school is public or private, and where it sits on the map. A business diploma at a public college in one province can cost a fraction of a professional degree at a research university in another city. Out-of-province and international student fees often run higher than in-province rates for the same credential.

Living costs sit beside tuition. Books, mandatory student fees, supplies, return trips home, childcare if you are a parent, and rent or residence fees can exceed tuition in expensive cities. Statistics Canada publishes current tuition averages by province on its website; your school’s fees page is the number that actually matters for your budget.

A degree that averages more than $80,000 over four years is not unusual once you combine tuition, fees, and living expenses. That figure is a benchmark, not a quote. Two students in the same city can face different totals because one lives at home and the other pays rent.

| Expense | Student A | Student B |

|---|---|---|

| Scenario | Lives at home, in-province college | Rents near campus, out-of-province university |

| Tuition and mandatory fees | ~$3,800 | ~$9,200 |

| Books and supplies | ~$1,200 | ~$1,400 |

| Housing and food | ~$2,000 (family contribution) | ~$14,000 |

| Transportation | ~$400 | ~$1,200 |

| Estimated academic-year total | ~$7,400 | ~$25,800 |

Take some time to do this calculation for yourself before applying to schools inside or outside your province. A student budget calculator from your bank or the school you’re applying to can help you get an idea of your total expenses per year. The earlier you know your funding gap, (the amount grants and savings will not cover) the more time you have to apply for aid and pick up summer work.

Student Financial Assistance Across Canada

Most Canadians access federal help through their province or territory. Quebec runs a separate system called Aide financière aux études (AFE). The application portal depends on where you live when you apply, (your province of residence).

The Federal Layer

The Government of Canada offers the Canada Student Grants and Canada Student Loans through provincial and territorial partners in every jurisdiction except Quebec, the Northwest Territories, and Nunavut. Federal aid is meant to cover up to 60% of your assessed financial need; your province or territory is expected to cover the rest through its own program.

Since April 1, 2023, Canada Student Loans charge no interest during your studies or after graduation. You repay only what you borrowed—no interest on top. For the 2026–2027 academic year, temporary federal investments will keep a 40% boost to non-repayable Canada Student Grants and raise the weekly Canada Student Loan cap from $210 to $300 per week of study.

Federal aid also carries lifetime limits: 340 weeks for most full-time students, 400 weeks for doctoral students, and 520 weeks for students with permanent disabilities. Certain professionals who work in under-served communities like, doctors, nurses, teachers, social workers, and early childhood educators, may qualify for federal loan forgiveness. Starting August 1, 2026, students at private for-profit international schools lose access to federal grants and loans. However, students already receiving aid at those schools may remain eligible until July 31, 2029 under a transitional rule.

Outside Quebec, your provincial portion is usually packaged with federal aid in one application; many students pay no interest on government loans while enrolled full time. However, since these rules change often, confirm the current policies on your province’s website.

Find Your Province or Territory Program

The following links will take you to the official provincial pages for student financial aid.

Provincial student aid opportunities change every year, and the mix of grant-to-loan support, career-college rules, and extra bursaries vary by province. Ontario is one example of that volatility: effective August 1, 2026, OSAP is shifting toward more repayable loans and less grant funding, and students at private career colleges will receive provincial OSAP entirely as loans.

Integrated Programs

British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Ontario, and Saskatchewan combine federal and provincial aid in one integrated application and repayment process.

Separate Programs

Alberta, Nova Scotia, and Prince Edward Island run provincial programs separately from the federal system but usually process applications at the same time.

Independent Programs

Quebec, the Northwest Territories, and Nunavut do not participate in the Canada Student Grants and Loans program at all.

Institutional Aid, Scholarships, and Other Sources

Your college or university may offer scholarships, bursaries, and awards based on merit, need, or both. As you review the different programs you would like to apply for, check out the financial aid opportunities at the college or university. Many deadlines fall months before classes start. Contact the student aid office at the college or university to clarify how to apply as a first-year student.

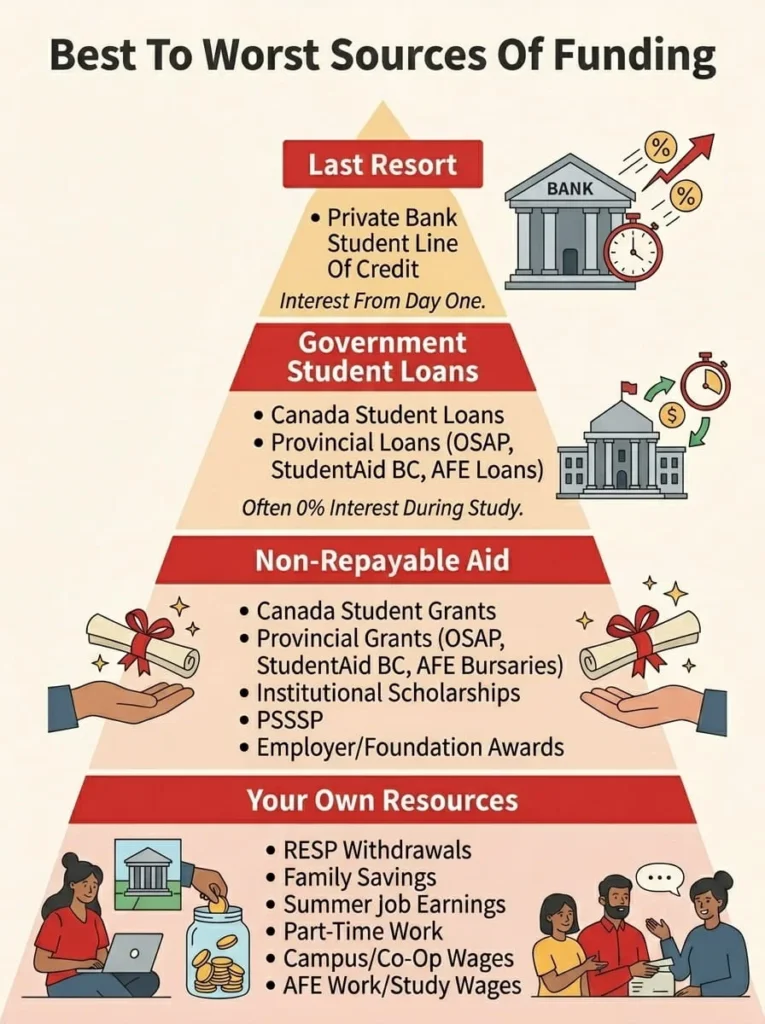

Beyond government programs, funding can come from financial institutions (student lines of credit), nonprofits, foundations, employer sponsorship, and Indigenous band or organization programs. Through the federal Post-Secondary Student Support Program (PSSSP), eligible First Nations students may receive up to $53,000 per year for standard studies or up to $90,000 for advanced professional degrees. Applications renew each academic year.

Many campuses hire students for part-time jobs or structured co-op and work-study-style roles. Rules differ by province and institution; your student aid office can explain what counts toward your package.

Private bank student lines of credit from lenders such as TD or CIBC fill gaps when government aid runs out. They are not interest-free. Interest starts the day you draw funds, and they do not qualify for government loan forgiveness. Treat them as a last resort after grants, RESP savings, and government loans.

AFE Loans and Bursaries

If you live in Quebec, you apply to AFE—not the Canada Student Grants and Loans program. During full-time study, the Quebec government pays the interest on an AFE loan while you remain enrolled. You borrow the loan amount itself; the province covers the interest during that period.

When full-time study ends, that is when you are expected to start repayment. AFE borrowers receive a notice from their financial institution about six months after their last study period. Interest may accumulate during that grace window; if you wait to start payments, that interest can be added to what you owe. The variable rate is the Bank of Canada preferential rate plus 0.50%. However, you may be able to negotiate a fixed rate with your bank, especially if you are proactive and start the process as soon as possible.

Quebec offers 15% loan remission for borrowers who studied full time, received an AFE bursary each year, and finished within the standard program timeline. Borrowers in hardship may apply for a Deferred Payment Plan with reduced payments over renewable six-month terms.

AFE Eligibility

AFE splits assistance into repayable loans and non-repayable bursaries based on your financial need, program, and enrollment status. To qualify for the Loans and Bursaries Program, you generally must study full time, stay below the debt limit for your program level, and show that your own resources are not enough to cover education costs.

AFE groups applicants by situation: students with parental or sponsor contributions, students with spousal contributions, and self-supporting students. Reported income is verified against Revenu Québec records after the school year. Maximum debt limits depend on your program type. For example, roughly $16,000 to $27,000 for college paths, $30,000 to $36,000 for many undergraduate degrees, and higher caps for graduate study or programs outside Quebec. Hitting your limit stops standard borrowing unless you file an exceptional-case request or change programs and get reassessed.

AFE Work/Study program

The AFE Work/Study Program helps students in precarious financial situations find employment at their educational institution. The program targets students whose budgets are tight enough that campus work could mean the difference between staying enrolled and dropping out.

Many Quebec schools also run co-op and practicum income streams. The standard AFE application includes a section for students in a full-time practicum, such as formal work-study or co-op placements. Elsewhere in Canada, campus employment plays a similar role, but subsidy rules and wage structures differ. Your financial aid office—not this lesson—owns those payroll details.

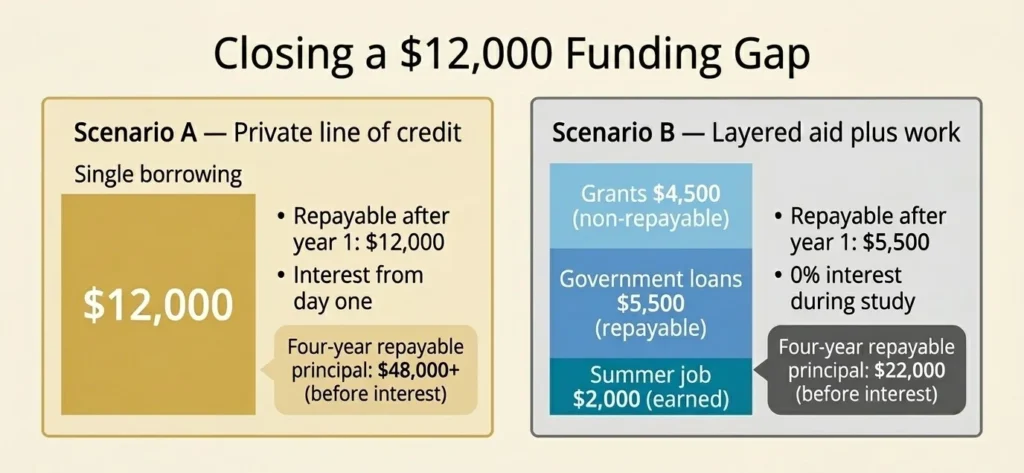

Comparing Funding Scenarios

Picture two first-year students each facing a $12,000 gap after tuition, fees, and living costs for one year. One student borrows the full amount on a private line of credit. The other pulls together grants, government loans, and summer job income. The side-by-side breakdown shows how each path changes what you owe—and for how long.

Start Your Funding Plan Early

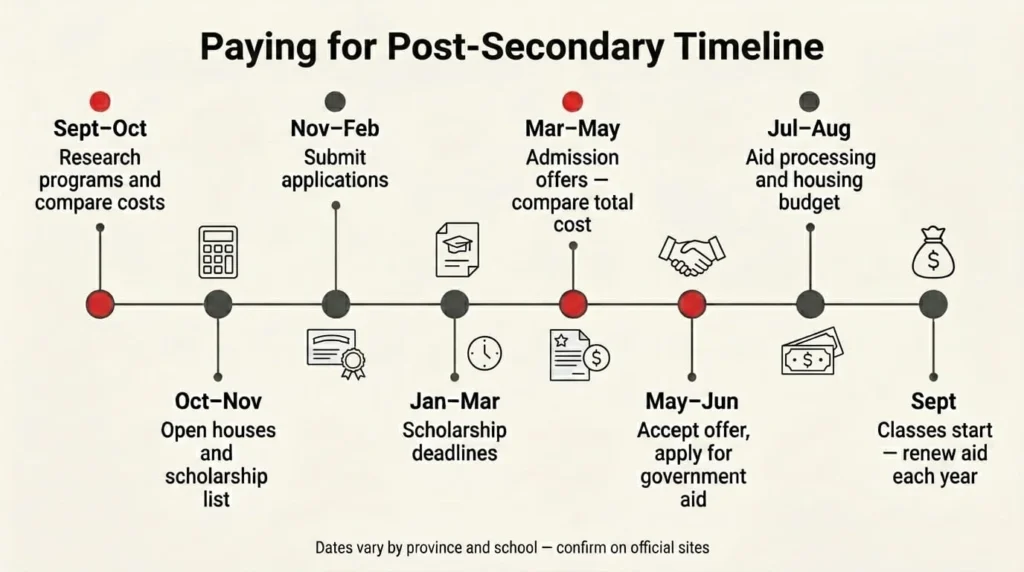

If you are in your final year of high school, start before you accept an offer or sign for loans. Research programs and compare what they cost where you actually want to study, (in your home province, another province, or away from home). Tuition, residence, and living expenses can look very different school to school.

Line up what you already have saved or that you will be able to save from part-time work or summer jobs, against those costs. That tells you your funding gap before you borrow. You can ask for help from your guidance counsellors at school about any scholarship options and deadlines to apply. Depending on your situation and the program you’re applying for, there might be institutional aid options. The deadlines for this funding are usually several months before classes start, so make sure you have your paperwork organized and ready to apply once you know where you’ll be studying.

Once you know where you are heading, apply for government aid through your province or territory’s portal (or AFE in Quebec). Applications typically open in the spring before your first year and must be renewed every academic year. Gather the documents your portal asks for—often tax information and program details—and allow several weeks for processing.

The goal is to have the least amount of student debt after you complete your degree. So, you’ll want to maximize non-repayable aid and RESP savings first, borrow only what you need through government programs, add earned income from campus or summer work, and reach for private credit only when all your other options are exhausted.