In Canada, safe and regulated banking products are widely available. When you understand how banks work, how deposits are protected, and how costly alternative financial services operate, you can make better financial choices and avoid debt traps.

Canada’s Financial System and Regulatory Structure

Canada’s financial system is one of the largest and most developed in the world. It includes five main types of financial institutions:

- Chartered banks: day-to-day banking (chequing/savings accounts), personal and business loans and mortgages.

- Trust and loan companies: historically specialized in trusts, estates and loan services.

- Co-operative credit unions and caisses populaires: member-owned alternatives to banks for everyday banking.

- Life insurance companies: life insurance, annuities, and related investment products for long-term saving.

- Securities dealers: buying/selling stocks, bonds, and other securities; investment advice and underwriting.

Market Concentration: The “Big Six”

The banking sector is highly concentrated. Six chartered banks: BMO, CIBC, TD, Scotiabank, RBC, and the National Bank, control roughly 70% to 90% of total banking assets. Credit unions and caisses populaires operate mainly under provincial rules. In some provinces, including Quebec, they serve about half the population. Several federal bodies oversee and protect the financial system.

Historical Development

In 1817, Canada’s first bank, the Bank of Montreal (BMO), opened. The banking system grew through a nationwide branch model. Banks could absorb regional shocks through a vast interprovincial branch network.

The system survived the Great Depression without major bank failures. No major chartered bank has failed since 1923. The Bank of Canada (BOC) was established in 1935, mainly in response to political pressure rather than economic need alone.

Federal Regulatory Oversight

The Department of Finance (DOF) sets broad policy to keep the whole system stable. The Bank of Canada (BOC) acts as the central bank. It supplies cash when banks need it and helps guide interest rates. The Office of the Superintendent of Financial Institutions (OSFI) regulates banks, insurers, and other financial firms. It checks that they hold enough capital and follow the rules. If a member bank fails, the Canada Deposit Insurance Corporation (CDIC) protects eligible deposits and takes over the institution. The Financial Consumer Agency of Canada (FCAC) enforces consumer protection rules. That includes clear fee disclosures and fair treatment when you deal with your bank.

A unique feature of Canada’s financial system is the “sunset clause.” Every five years, Parliament must review and update the Bank Act. These reviews give lawmakers a regular chance to revise banking rules.

Major legislative milestones include:

- 1954: Banks were authorized to issue government-insured mortgages and personal chattel loans.

- 1967: The 6% interest rate ceiling on loans was removed, opening the door to competitive commercial lending.

- 1987: Legislative changes removed the equivalent of the United States Glass-Steagall Act, permitting banks to own securities dealers.

- 2018: Amendments allowed banks to invest in or form partnerships with financial technology (fintech) corporations.

Maintaining Financial Stability

Federal law limits how much debt banks can carry and how much they can lend against residential property. Together, these rules help keep the system stable.

Leverage Limits

By law, a bank can hold assets up to 20 times its capital. Regulators may allow up to 23 times with approval. That keeps average bank leverage around 18:1, lower than the roughly 25:1 typical in the United States.

Mortgage Rules

Your loan-to-value ratio is how much you borrow compared to the home’s price. If you borrow more than 80% of the home’s value, federal rules require mortgage default insurance from the Canada Mortgage and Housing Corporation (CMHC) or a private insurer.

Federally regulated banks also cannot approve a residential mortgage above 95% loan-to-value — so you need at least a 5% down payment.

Choosing the Right Account

Account types differ in fees, transaction limits, and deposit coverage. The Canada Deposit Insurance Corporation (CDIC) is the main federal protection for bank deposits. CDIC automatically insures deposits up to $100,000 for each type of eligible account you hold at the bank if a member institution fails.

You can also choose to bank with Indigenous-owned financial institutions. Indigenous-controlled banks and trust companies—such as the First Nations Bank of Canada and Peace Hills Trust—offer culturally responsive credit options and banking services to support communities across the country, serving as reliable alternatives to chartered banks and credit unions.

Eligible Deposits Include:

- Deposits held in one name

- Joint deposits (held in more than one name)

- Trust deposits

- Registered Retirement Savings Plans (RRSPs)

- Registered Retirement Income Funds (RRIFs)

- Tax-Free Savings Accounts (TFSAs)

- Registered Education Savings Plans (RESPs)

- Guaranteed Investment Certificates (GICs)

- Deposits held in Canadian or foreign currencies

Not every financial product is covered, so the CDIC protection does not apply to:

- Mutual funds

- Stocks

- Bonds

- Exchange Traded Funds (ETFs)

- Cryptocurrencies

When you choose an account, think about your banking habits. Different accounts offer different transaction limits, fees, and features. You want to match the account to how often you deposit, withdraw, and pay bills.

For example, TD Canada Trust offers several chequing accounts you can compare:

| Account | Monthly Fee | Transaction limit |

|---|---|---|

| Minimum Chequing Account | $3.95 per month | Up to 12 transactions |

| Every Day Chequing Account | Standard monthly fee | Up to 25 transactions |

| Unlimited Chequing Account | Higher monthly fee | Unlimited transactions |

| Student Chequing Account | $0 monthly fee | Unlimited transactions |

Banking Skills, Payments, and Transfers

Modern banking did not appear overnight. Over decades, new tools made it easier to access your money on your own schedule — without visiting a teller or waiting for a paper cheque.

- 1957: Personal chequing accounts became widely available, making everyday banking normal for households.

- 1972: Automated banking machines (ABMs) let you transfer funds and pay bills around the clock.

- 1986: The national Interac ABM network connected machines across the country, so you could bank far from your home branch.

Today, more than 18,700 ABMs process hundreds of millions of transactions each year. One of the most practical banking skills is using direct deposit. Instead of relying on cheque-cashing services, you can have payroll deposits and government benefits sent directly into your bank account. For government benefits you can login to your Canada Revenue Agency or Service Canada portal to input your details.

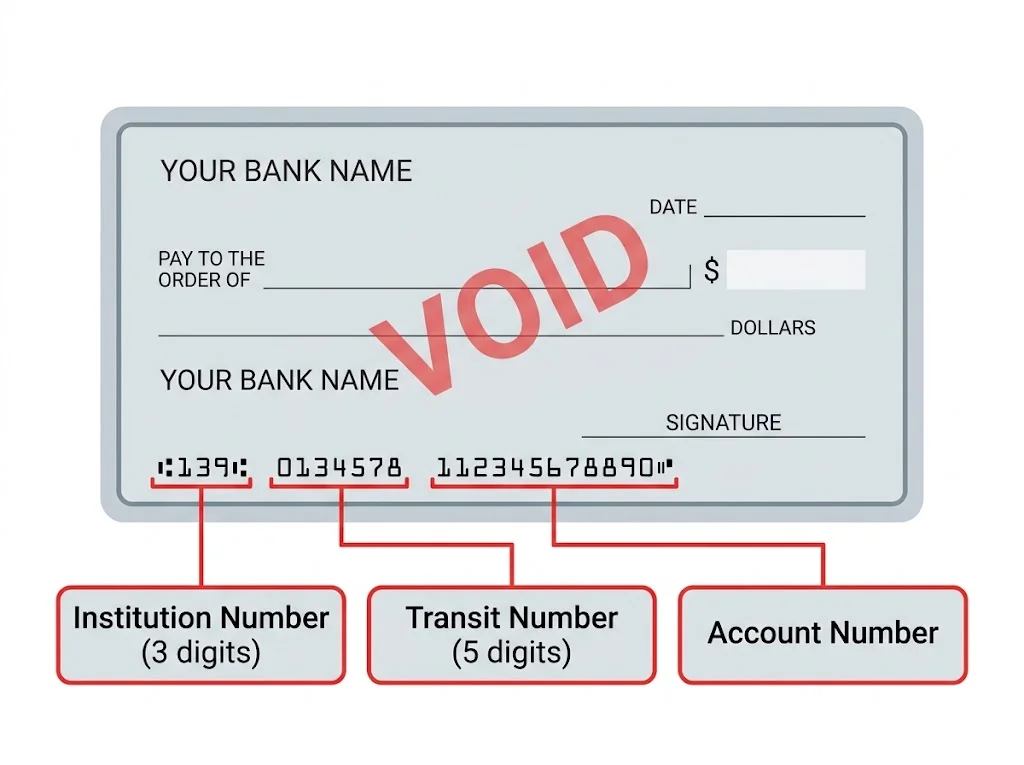

To set up direct deposit safely, you’ll need your account’s routing numbers: your three-digit institution number, your five-digit transit number, and your unique account number. You can get these by downloading a pre-filled direct deposit form from your online banking portal, or by writing “VOID” across a physical paper cheque to prevent unauthorized withdrawals while still displaying your routing codes.

You may be asked to bring a void check or send a copy to your HR department or someone from the payroll so they can set-up direct deposit for you.

Government of Canada Cheque-Cashing Rights

By law, you have a right to cash Government of Canada cheques free of charge at any retail bank, subject to the following limits:

- The cheque value must be $1,750 or less.

- The transaction must not be suspected of fraud.

- You must present either two reliable pieces of identification (one showing your name and current address, and one showing your name and date of birth) OR one piece of government-issued photo identification that includes your signature.

Digital Money Transfers: Interac e-Transfer

To send an Interac e-Transfer, you enter the recipient’s name, email address, and transfer instructions from within your online bank account. If the recipient has registered for “auto-deposit,” funds arrive immediately without a security question or password. Many people use e-Transfer for large one-time payments, such as university tuition.

Banking in the Digital Age

Banking has continued to evolve alongside technology.

- 1995: Launch of the first Canadian bank website.

- 1996: Introduction of internet banking platforms.

- 2010: Deployment of the first mobile banking app.

Today, you can check your bank balances, transfer money, pay bills, and manage your money directly on your smartphone while anywhere in the world. Banks have also introduced biometric security, such as eye and facial recognition to protect your account from hackers.

While online banking has made it easier to access your money from anywhere, it’s also presented new risks. You need to watch out for common scams that trick you into sharing information scammers can use to access your bank account. You could be exposed to sophisticated digital scams, or a technical issue, like forgetting for password can lock you out of your funds with no immediate in-branch support to resolve the issue.

Phishing and Smishing

Fraudulent emails (phishing) and text messages (smishing) mimic real financial institutions. These attacks target credit card numbers, online banking passwords, and Social Insurance Numbers (SINs). Legitimate banks do not ask for account passwords or login details by email.

Fintech and Crypto Risk

Amendments to the Bank Act in 2018 let banks invest in and partner with fintech companies. However, any money or cryptocurrency you keep in digital investing apps is not protected by CDIC deposit insurance. You must be careful when using online brokerage accounts or other investing apps, because your money is not safe if the company goes bankrupt or shuts down. Some platforms pull off “exit scams” where they freeze withdrawals, mix your cash with their own, and disappear with your funds. Other projects use “rug pulls” to suddenly drain all the money out of a token and leave you with worthless assets.

High-Cost Financial Services and Consumer Protection

Many people on low or tight incomes turn to alternative financial services because they seem convenient when they need cash immediately. These include payday loans, instalment loans, pawn loans, title loans, and rent-to-own contracts.

These options may solve a short-term problem, but they often carry heavy costs.

For example, rent-to-own stores can charge up to four times the standard retail price of an item. What looks affordable at first can become extremely expensive over time. Cheque-cashing outlets can also shrink your paycheque. Some charge up to $3.50 plus 3.5% of a cheque’s value just to access money that already belongs to you.

These costs can trap you in a cycle of paying fees to access income or borrow funds. That makes it harder to build financial stability.

Legislative Interventions and Policy Recommendations

Section 347 of the Criminal Code sets Canada’s criminal interest rate—the maximum a lender can legally charge before the loan becomes a criminal offence. From 1980 until the end of 2024, that cap stood at 60% per year. Groups including ACORN Canada, the Public Interest Advocacy Centre (PIAC), and Momentum argued for years that the limit was too high. They called for lowering it to 30% or 36% to better protect borrowers who rely on installment and payday loans.

Federal lawmakers acted on part of that pressure. As of January 1, 2025, the criminal interest rate is 35% annual percentage rate (APR) on most consumer loans. Some loan types, including certain commercial, pawn, and payday loans, follow separate rules with different limits.

In a 2021 policy paper endorsed by more than 30 anti-poverty, tenant, and labour groups, ACORN Canada, PIAC, and Momentum also pushed for hard caps on cheque-cashing fees, rules requiring employers to offer direct deposit, price limits and contract reinstatement rights on rent-to-own deals, and requirements that lenders check whether you can repay before extending credit. They have also urged chartered banks to widen access to basic accounts and affordable small-dollar credit as safer alternatives to fringe lenders.

Protecting Yourself and Your Money

Financial safety involves more than choosing the right account. You should also know how to spot counterfeit currency. One recommended approach is the feel-look-tilt method.

Feel

Check the texture and security features of the banknote.

Look

Inspect visible security elements.

Tilt

Observe how security features change when you tilt the note.

These steps help you spot suspicious currency.

Protecting your money is an ongoing habit, not a one-time check. Along with staying alert to scams and counterfeit cash, good banking habits require you to understand common fee terms.

An overdraft occurs when your bank allows you to spend more money than you actually have in your account, treating the difference as a costly short-term loan. If you try to write a cheque or make a pre-authorized payment without enough money in your account, the payment will bounce. The bank rejects the transfer and hits you with a Non-Sufficient Funds (NSF) fee, which can easily cost over $40 per transaction. Reviewing your balances regularly prevents these unnecessary expenses.

Good banking habits include reviewing your account activity regularly, understanding the fees you pay, using overdraft protection sparingly, and choosing accounts and products that fit how you actually earn, spend, and save.